Filing a flat roof insurance claim Toronto homeowners can actually win takes more than a phone call to your broker after a storm. With hail events, derecho-style wind gusts and freeze-thaw cycles intensifying across the GTA in 2026, low-slope roofs on Toronto, Mississauga, Markham and Vaughan homes are absorbing real punishment. Yet many claims get reduced or denied because the damage is misclassified as “wear and tear” rather than a sudden insured peril. This guide walks you through how payouts work, what documentation adjusters expect, realistic 2026 cost figures, and how to protect your right to a fair settlement on a TPO, EPDM, modified bitumen or PVC roof.

At Flat Roofs Toronto, our crews are called in after nearly every major GTA storm to inspect, document and repair flat roofs for homeowners navigating the claims process. The patterns are predictable, and so are the mistakes that cost people thousands. Read this before you call your insurer.

How a Flat Roof Insurance Claim in Toronto Actually Works

A standard Ontario home insurance policy covers your flat roof against “named perils” or “all perils” depending on your coverage tier. The key distinction for a flat roof insurance claim Toronto adjusters will scrutinise is whether the damage was caused by a sudden, accidental event (covered) or by gradual deterioration, poor maintenance or aging (excluded). Hail, windstorm, falling tree limbs and ice-related water entry are typically covered perils. A membrane that has simply reached the end of its service life is not.

When you report damage, your insurer assigns a claims adjuster who inspects the roof, reviews your policy, and determines the payout. On most GTA policies, roofs are settled on either a Replacement Cost Value (RCV) or Actual Cash Value (ACV) basis. RCV pays what it costs to rebuild new; ACV subtracts depreciation for the age of the roof. Knowing which one applies to your policy before disaster strikes is the single most important thing you can do.

Most insurers in 2026 also apply a roof-age schedule. Once a flat roof passes 15 to 20 years, many carriers automatically shift coverage from RCV to ACV, or exclude roof surfacing entirely. This is why a professional assessment from a licensed flat roofing contractor, separate from the insurer’s adjuster, is worth its weight in gold.

| Settlement Basis | What It Pays | Typical Trigger | Homeowner Impact |

|---|---|---|---|

| Replacement Cost Value (RCV) | Full cost to replace with new materials | Roof under ~15 years, well maintained | Best outcome; minimal out-of-pocket beyond deductible |

| Actual Cash Value (ACV) | Replacement cost minus depreciation | Older roof or basic policy tier | Large gap you must fund yourself |

| Repair-only settlement | Cost to patch affected area only | Localised, isolated damage | Fine for small claims; risky if damage is widespread |

| Denied claim | Nothing | Damage ruled wear and tear or pre-existing | Appeal or fund repair yourself |

Common Storm Damage to GTA Flat Roofs and Whether It Is Covered

Flat and low-slope roofs fail differently than pitched shingle roofs, and adjusters who specialise in steep-slope work sometimes misjudge them. Understanding the failure modes helps you describe damage accurately on your claim and push back on an unfair assessment.

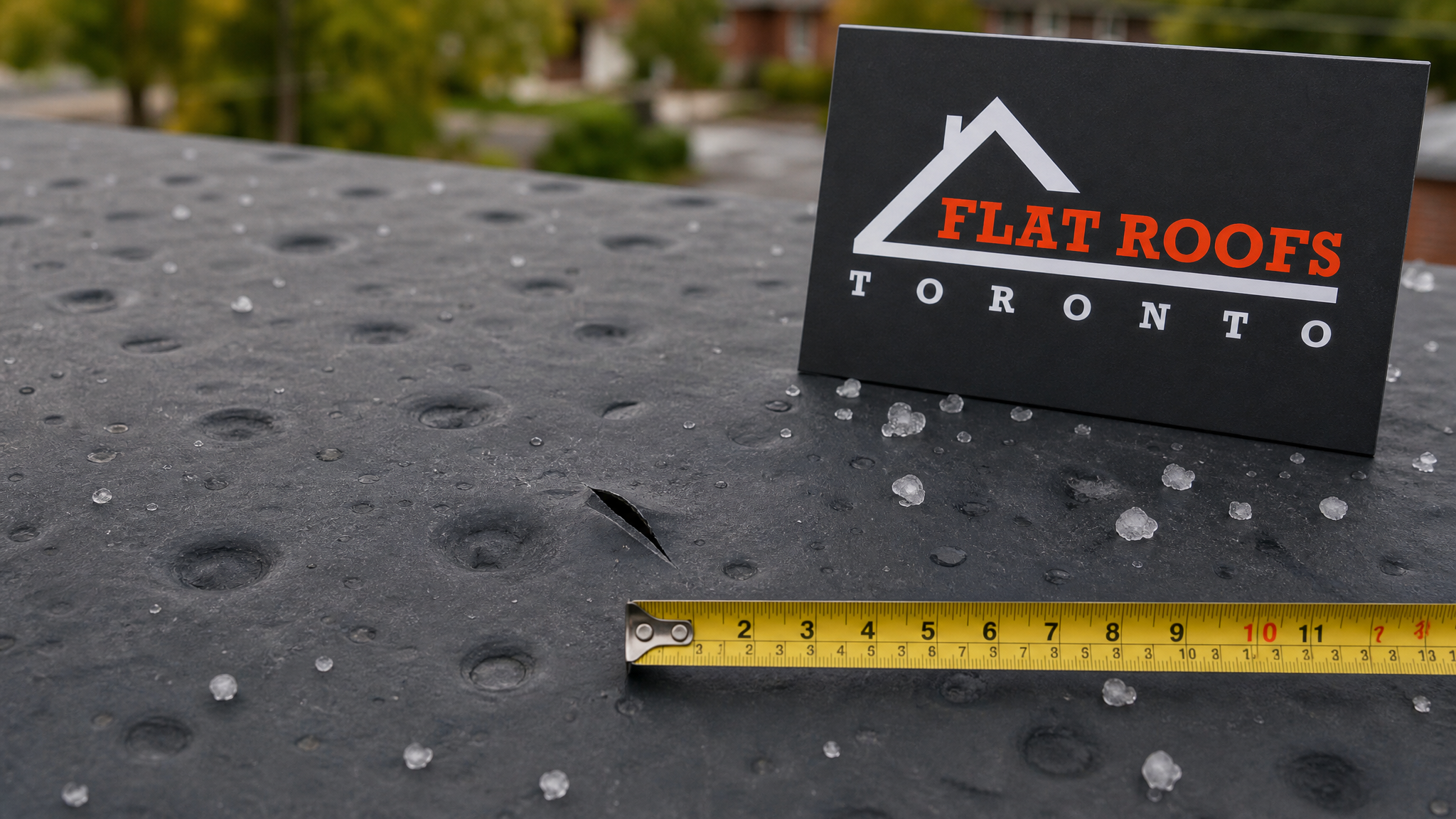

Hail bruises and fractures membranes. On EPDM (rubber) it leaves circular impact marks and can split the sheet; on modified bitumen it dislodges the granular surface and exposes the asphalt to UV. Wind lifts and peels membrane edges, tears flashing, and strips ballast or pavers off the field of the roof. Falling debris from trees punctures the membrane outright. Ice and freeze-thaw drives water under seams, then expands and ruptures them, often showing up months later as interior staining.

If you are unsure whether damage qualifies as a sudden peril, an emergency inspection from our emergency roof repair team can document the cause before the evidence weathers away. Timing matters: insurers expect prompt reporting, and a roof left open invites secondary water damage they may refuse to cover.

| Damage Type | How It Appears on a Flat Roof | Usually Covered? | Documentation Needed |

|---|---|---|---|

| Hail impact | Bruising, granule loss, membrane splits | Yes, as a sudden peril | Dated photos, Environment Canada hail report |

| Wind uplift | Peeled edges, torn flashing, missing ballast | Yes, with wind-speed evidence | Weather records, edge-detail photos |

| Tree or debris impact | Punctures, crushed insulation | Yes | Photos of debris in place, removal receipts |

| Ponding water / drainage | Standing water, blistering over time | Often denied (maintenance) | Hard to claim unless storm-caused |

| Aged seam failure | Open laps, no impact marks | No (wear and tear) | Not claimable |

The Claims Timeline: What to Expect Week by Week

A typical GTA flat roof claim moves through predictable stages, though peak post-storm volume can stretch every step. After the 2026 spring hail events, many Toronto and Mississauga adjusters were booking inspections two to three weeks out. The faster you report and document, the faster you move through the queue.

| Stage | Typical Timeline (GTA 2026) | Your Action Item |

|---|---|---|

| Report claim to insurer | Within 24-72 hours of damage | File immediately; get a claim number |

| Emergency mitigation / tarping | Same day to 48 hours | Stop water entry; keep all receipts |

| Adjuster inspection | 3-21 days after reporting | Have your own contractor report ready |

| Estimate and approval | 1-3 weeks after inspection | Compare insurer estimate to a real quote |

| Repair / replacement | 2-8 weeks depending on scope | Use a licensed flat roofing contractor |

| Final payment release | After work completed (RCV holdback) | Submit final invoice and photos |

Note the RCV holdback in the final row. On replacement-cost policies, insurers often pay the depreciated amount up front and release the remaining “recoverable depreciation” only after you prove the work was completed. This means you cannot simply pocket the cheque and skip the repair without losing money.

2026 Flat Roof Repair and Replacement Costs in the GTA

Knowing real numbers protects you when an adjuster’s estimate comes in low. Costs vary by membrane type, roof size, access difficulty and how much substrate or insulation was damaged. The figures below reflect 2026 pricing across Toronto, Mississauga, Markham and Vaughan for residential and small-commercial flat roofs. Use them to sanity-check any settlement offer.

| Scope of Work | Membrane / Detail | 2026 GTA Cost Range | Notes |

|---|---|---|---|

| Emergency tarp / temporary patch | Any | $350 – $900 | Reimbursable mitigation expense |

| Localised storm repair | EPDM / modified bitumen | $800 – $2,500 | Single puncture or seam section |

| Partial membrane replacement | TPO / PVC | $4,000 – $9,000 | One field section plus flashing |

| Full residential flat roof replacement | TPO (heat-welded) | $9,000 – $22,000 | Includes tear-off and new insulation |

| Full replacement with skylight reset | PVC + curb reflashing | $14,000 – $30,000+ | Larger or multi-level roofs |

If your roof needs full replacement, this is the moment to consider an upgrade. Our residential flat roof installation services use heat-welded TPO and PVC systems that hold up far better to GTA hail and wind than older two-ply built-up roofs. For multi-unit or mixed-use buildings, commercial flat roof installation follows the same insurance-friendly documentation standards.

Documentation That Wins Claims (and Mistakes That Lose Them)

The difference between a full payout and a denied claim is almost always documentation. Adjusters work from evidence, not your word. Build your file before, during and after the storm.

Before damage: keep dated photos of your roof in good condition, retain your installation invoice and any maintenance records, and know your policy’s roof-age clause. A maintained roof with a paper trail is far harder to dismiss as neglected.

Immediately after: photograph everything from multiple angles, including wide shots that establish context and close-ups of impact marks, torn flashing or debris. Capture the date stamp. Save the Environment Canada weather record for the storm date, which corroborates that a covered peril occurred. Do not throw away fallen branches or torn membrane until the adjuster has seen them or you have photos.

During mitigation: stop further water entry, but keep all receipts for tarps, emergency repairs and any interior cleanup. These are reimbursable and also prove you acted responsibly to limit the loss, which is a policy obligation.

The most common claim-killer we see at Flat Roofs Toronto is the homeowner who lets weeks pass, then reports vaguely defined leaking. By then the membrane has weathered, the storm correlation is harder to prove, and the adjuster classifies it as a maintenance issue. Speed and specificity protect your money.

Working With the Adjuster and Disputing a Low Offer

When the adjuster arrives, be present, be organised, and have your own contractor’s inspection report in hand. An independent assessment from a flat roofing specialist often catches damage a generalist adjuster overlooks, such as compromised insulation under an intact-looking membrane or seam separation that will leak within a season.

If the insurer’s estimate is lower than realistic repair costs, you have options. First, request the adjuster’s itemised scope and compare it line by line to a quote from a licensed contractor. Second, ask your contractor to submit a supplemental estimate documenting overlooked items. Third, if you still disagree, Ontario policies include an appraisal clause that lets each side appoint an appraiser and, if needed, a neutral umpire to settle the dollar figure without litigation.

Two practical cautions. Avoid “storm chaser” contractors who appear door to door promising to cover your deductible, which is insurance fraud in Ontario. And do not sign an “assignment of benefits” form that hands your claim rights to a contractor before you understand it. A reputable local company works transparently alongside you and your insurer.

| Situation | Recommended Action | Why It Helps |

|---|---|---|

| Offer below repair cost | Submit contractor supplemental estimate | Forces documented re-evaluation |

| Damage ruled wear and tear | Provide maintenance records and storm date evidence | Reframes as sudden peril |

| Stalemate on amount | Invoke policy appraisal clause | Binding resolution without court |

| Denial you believe is wrong | Escalate to GIO / FSRA ombudsman | Independent review of insurer conduct |

Preventing the Next Claim: Resilient Flat Roofing Upgrades

The best insurance claim is the one you never have to file. After a storm settlement funds a new roof, build in resilience so the next hail event is a non-event. Heat-welded TPO and PVC membranes resist puncture and uplift better than aged built-up systems, and properly detailed flashing keeps wind from finding an edge to peel.

Upgrades that pay off in the GTA climate include reinforced membrane in high-impact zones, improved drainage to eliminate ponding, and added attic insulation to reduce the ice-damming and condensation that quietly degrade flat roofs from below. If your roof has skylights, storm season is the right time to reseal or replace them; our residential skylight and commercial skylight teams integrate curb flashing into the membrane so the most leak-prone detail on your roof is also the strongest. You can see completed resilient installations in our project gallery.

An annual professional inspection, ideally each spring and after any major storm, also creates the maintenance record that keeps your insurer on the Replacement Cost Value schedule rather than dropping you to depreciated coverage.

How long do I have to file a flat roof insurance claim in Toronto?

Will my insurance cover an older flat roof?

What is the difference between RCV and ACV on a roof claim?

My claim was denied as wear and tear. Can I dispute it?

Should I get my own inspection before the adjuster visits?

Who pays my deductible after a storm claim?

Get Help With Your Flat Roof Insurance Claim in Toronto Today

Storm season in the GTA is unforgiving, but a well-documented claim and a resilient new roof put you back in control. Whether you need emergency tarping, an independent damage report for your adjuster, or a full replacement once your settlement clears, Flat Roofs Toronto guides Toronto, Mississauga, Markham and Vaughan homeowners through every step of the process with honest pricing and insurance-ready documentation.

Call us today at (647) 333-3528 or request a free flat roof quote to schedule a storm-damage inspection and protect your payout.

Flat Roofs Toronto proudly serves homeowners across Toronto, Mississauga, Markham, Vaughan and the wider GTA with expert flat roofing repair, replacement and insurance claim support.